News Trends

【World Express】Fuji Keizai Releases 2026 Report: From Si to SiC to Ga₂O₃, Power Semiconductors Enter a Multi-Generational Parallel Evolution Phase

日期:2026-04-29阅读:691

Recently, Fuji Keizai released a new report on the global power semiconductor market, providing a systematic analysis of industry development trends and future outlook.

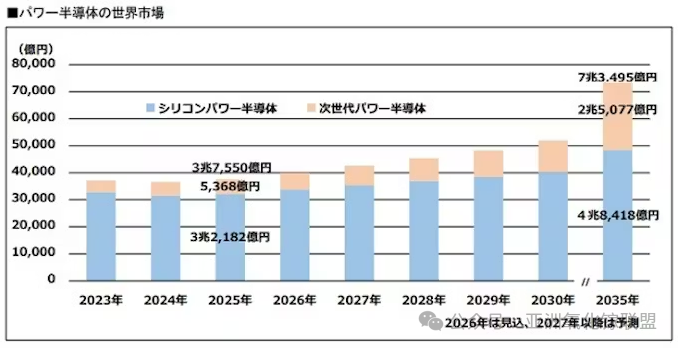

According to the report, the global power semiconductor market is expected to reach approximately 7.35 trillion yen (about 314.6 billion RMB) by 2035, representing an increase of around 95.7% compared with 2025. However, this growth will not be linear, but rather characterized by clear cyclical fluctuations. In the short term, growth is weakening due to a slowdown in electric vehicle (EV) expansion, which has reduced demand in automotive electronics. At the same time, inventory adjustments and capacity expansion from previous years are still being absorbed, keeping the industry in a relatively soft adjustment phase. Nevertheless, demand recovery in some consumer electronics and information and communication devices continues to support modest growth in silicon-based power semiconductors.

From a medium-term structural perspective, the industry’s growth logic is undergoing a noticeable shift. As AI server power density continues to increase, data centers are placing significantly higher demands on power conversion efficiency. As a result, demand for power semiconductors is gradually shifting away from “EV-driven electrification” toward “computing infrastructure and energy efficiency optimization.” This transition means that market growth is becoming less dependent on a single application sector and increasingly driven by system-level efficiency improvements.

At the material level, this trend is even more evident. Silicon-based power devices still form the market foundation, but growth momentum is increasingly concentrating on wide bandgap materials. Among them, silicon carbide (SiC) power devices have entered a phase of large-scale deployment, continuing to replace IGBTs in key applications such as EV traction inverters, while also expanding into energy storage and photovoltaic systems. However, as capacity expands and more players enter the market, price competition is intensifying, shifting the growth logic from “technology-driven premium pricing” to “mass adoption driven by scale.”

Gallium nitride (GaN), on the other hand, is following a different trajectory. Initially driven by the consumer electronics fast-charging market, it is now expanding into on-board chargers, AI server power supplies, and high-frequency communication and sensing systems, evolving from a consumer-level device into a system-level power technology.

In contrast, gallium oxide (Ga₂O₃) remains at an early stage, with the market size still close to zero. However, it is gradually moving from the validation phase toward early commercialization, with its technological pathway becoming increasingly clear. Around 2027, 600V-class Schottky barrier diodes (SBDs) are expected to enter mass production and begin adoption in power supply applications, laying the foundation for future scaling. From a material perspective, gallium oxide offers strong potential due to its ultra-wide bandgap and extremely high breakdown voltage, making it attractive for high-voltage, high power-density applications. Although the rapid cost reduction of SiC is partially eroding its original cost advantage, gallium oxide still retains differentiated potential in higher-voltage and more extreme power applications. By around 2030, as transistor devices mature, its applications are expected to extend into industrial energy systems and megawatt-level power conversion. Overall, gallium oxide is increasingly viewed as a potential next-generation high-voltage power device technology, with its long-term growth trajectory depending on progress in industrialization.